Circular Debt Pakistan: Impact on Your Electricity Bill

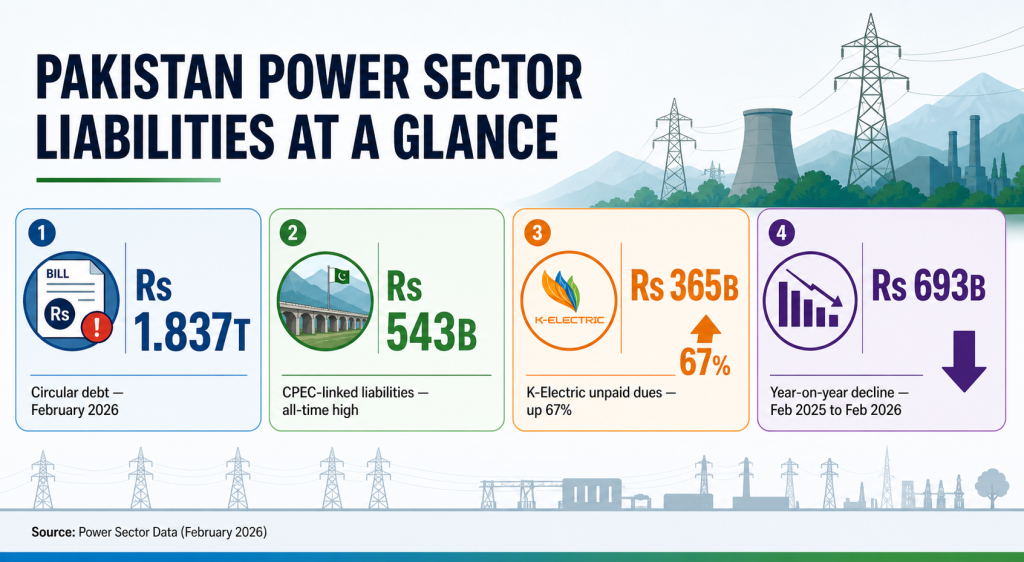

Circular debt in Pakistan is no longer just a term economists use in reports. It is the reason your electricity bill carries charges you never agreed to pay. As of February 2026, this debt stands at Rs 1.837 trillion in the power sector alone. That figure affects every household connected to the national grid, every factory running a production line, and every small shop whose owner already struggles with inflation. Understanding what drives this debt, and what the government is actually doing about it, is no longer optional for anyone who pays an electricity bill in Pakistan.

This article covers every layer of the crisis: the debt’s structure, its root causes, the burden it places on ordinary Pakistanis, and the government’s reform effort in 2026.

What Is Circular Debt?

What is circular debt in Pakistan? Circular debt in Pakistan is a chain of unpaid dues across the power supply chain, where distribution companies cannot pay power producers, and power producers cannot pay fuel suppliers. And the government borrows to fill each gap, adding those borrowing costs to consumer electricity bills. As of February 2026, Pakistan’s power sector circular debt is down from a peak of Rs 2.636 trillion in 2024, but is still growing month-on-month.

Circular Debt Pakistan 2026: Where the Numbers Stand Today

Pakistan’s circular debt stands at Rs 1.837 trillion as of February 2026, according to data compiled by Arif Habib Limited and the Ministry of Energy. This is down from a peak of Rs 2.636 trillion in 2024 but up Rs 224 billion from June 2025. It is showing that the debt is still accumulating despite restructuring efforts.

The IMF acknowledged this as “significant progress” and noted that industrial electricity demand rose 35% year-on-year between April and August 2025, which helped DISCOs collect more revenue. That improvement was real but incomplete.

By February 2026, the debt had climbed back to Rs 1.837 trillion, adding Rs 224 billion in just eight months. The Power Division attributes this to seasonal factors and timing differences in payments. Zafar Masud, Chairman of the Pakistan Banks Association, framed the situation plainly after the September 2025 restructuring deal. The stock was resolved at a point in time, but the flow of new debt accumulating every month was never stopped. His warning holds: Pakistan’s power sector keeps generating fresh losses faster than governance reforms can seal the leaks.

NEPRA’s State of Industry Report FY 2024–25, the regulator’s official annual audit of DISCOs, was released in January 2026. It puts a precise figure on DISCO failure: weak distribution performance added Rs 397 billion to circular debt that year alone. Of that, Rs 265 billion came from losses exceeding NEPRA’s permitted targets, and Rs 132 billion from under-recoveries. The five worst performers were KE, PESCO, HESCO, SEPCO, and QESCO. NEPRA’s own conclusion: except for TESCO, not a single DISCO met its regulator-approved T&D loss target for the year.

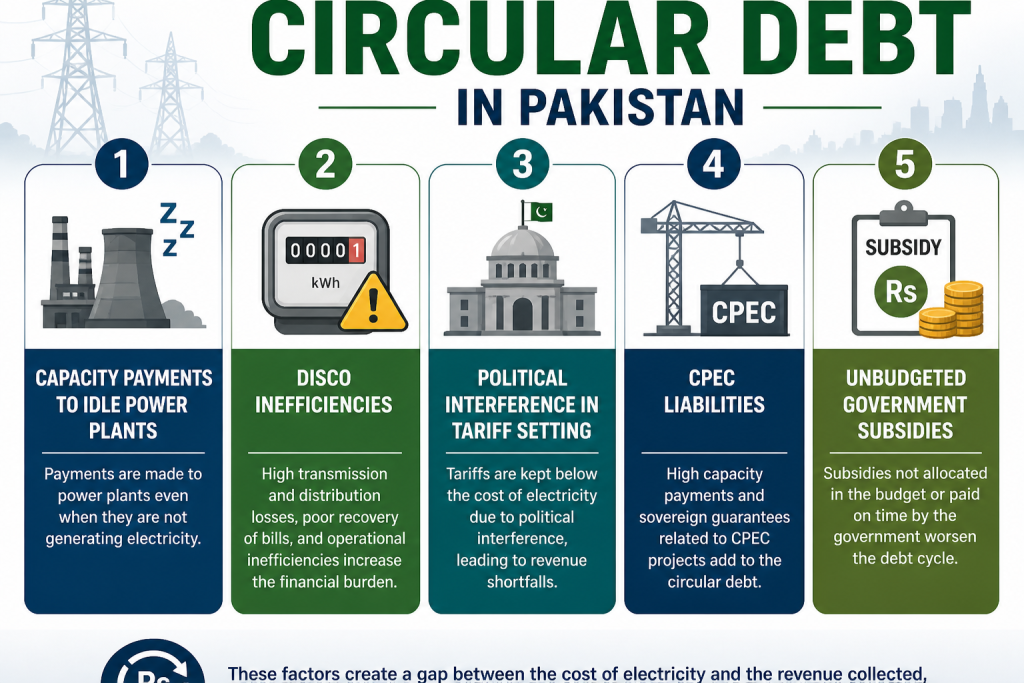

Five Causes Driving Pakistan’s Power Sector Debt

The five main causes of circular debt in Pakistan are capacity payments to idle power plants, DISCO inefficiencies, political interference in tariff setting, CPEC liabilities, and unbudgeted government subsidies.

Capacity payments to idle power plants

Pakistan pays IPPs a guaranteed fee called a capacity payment, whether they generate electricity or not. With 45,888 MW of installed capacity but a peak utilisation rate of just 34%, consumers effectively fund idle infrastructure. Total annual capacity payments crossed Rs 2.1 trillion by 2024. These payments represent Pakistan’s third-largest national debt obligation, after defence and foreign debt.

Read Also: What are Capacity Charges in Pakistan?

DISCO inefficiency and electricity theft

DISCOs lose 16–17% of all electricity they distribute through transmission and distribution (T&D) losses, far above the international benchmark of 5–8%. Theft through illegal “kunda” connections, inflated billing, and low metering accuracy compound the problem. In FY 2024–25, under-recoveries alone added Rs 132 billion to the debt stock.

Political interference in tariff setting

NEPRA determines electricity tariffs based on actual generation costs. But governments regularly delay notifying those tariffs, sometimes by 9 to 12 months, because tariff hikes create political backlash. During the delay, the gap between what electricity costs and what consumers pay widens. DISCOs absorb that gap as losses. Those losses compound into circular debt.

CPEC power project liabilities

Chinese IPPs under CPEC carry a 75% debt-to-equity ratio and guaranteed equity returns of 27–34%, far above global norms. Their contracts contain dollar indexation clauses, which means every time the rupee depreciates, the government’s payment obligation rises without a single extra kilowatt being generated. CPEC-linked liabilities hit a record Rs 543 billion in February 2026 and remain the hardest part of the debt to renegotiate.

Unbudgeted subsidies paid late or not at all

The government commits to subsidising tariff differentials for lower-income consumers. But these subsidies frequently arrive late, or the budgeted amount falls short of what is owed. Each shortfall adds directly to the debt the government owes power producers. In FY 2025–26, subsidy allocations were cut from Rs 1.19 trillion to Rs 1.04 trillion under IMF conditions, tightening cash flow further.

How Pakistan’s Electricity Crisis Hits Your Monthly Bill?

Pakistan’s electricity crisis does not stay inside government ledgers. It converts every trillion rupees of accumulated debt into rupees-per-unit charges that every connected household pays, regardless of how efficiently they use electricity.

Read Also: Why Electricity Bills Are High in Pakistan

The Debt Service Surcharge: Rs 3.23 Per Unit You Pay for Old Debt

In September 2025, the government completed the largest financial transaction in Pakistan’s history, securing Rs 1.225 trillion from 18 commercial banks to restructure the circular debt stock. The deal restructured Rs 660 billion in existing loans and raised Rs 565 billion in fresh financing to settle IPP dues, all at the concessional rate of KIBOR minus 0.9%. To repay this over six years in 24 quarterly instalments, NEPRA added a Debt Service Surcharge of Rs 3.23 per unit to every electricity bill.

A household consuming 300 units a month pays Rs 969 per month — Rs 11,628 per year purely through this surcharge, before accounting for the base tariff, fuel adjustments, or taxes. That is money going not toward the electricity you use, but toward debt accumulated before you started paying.

What Rs 3.23/unit actually costs households:

200 units/month → Rs 646/month extra | 300 units/month → Rs 969/month extra | 500 units/month → Rs 1,615/month extra

Every consumer pays this surcharge for six years regardless of their income level.

The Regressive Burden: Why Poor Households Pay Proportionally More

Circular debt does not harm everyone equally. PIDE research (Knowledge Brief No. 2025:135, Dr. Rubina Ilyas) shows that 30–35% of the current electricity tariff consists of non-energy financial charges, debt repayment, surcharges, and inefficiency costs. For the poorest 40% of households, this share climbs to 55–60% of their total bill.

“Converting unpaid liabilities into additional levies on units turns cost-recovery into a regressive mechanism — hitting poor households hardest and delivering little fiscal relief.”— Dr. Rubina Ilyas, Research Economist, PIDE, October 2025

A low-income family consuming 100 units a month pays Rs 22.44 per unit, of which nearly 37% covers debt-related charges, not energy. A wealthy household consuming 700+ units pays a higher absolute bill but carries a much smaller debt share proportionally. Meanwhile, the richest consumers are buying solar panels and exiting the grid entirely, shrinking the revenue pool and pushing costs further onto those who cannot afford to leave.

Pakistan Energy Sector Reforms in 2026: What Is Actually Moving

Pakistan energy sector reforms in 2026 operate on three parallel tracks: debt restructuring, DISCO privatisation, and IPP contract renegotiation. Each track has shown some progress. None has resolved the structural causes of the debt.

DISCO Privatisation: Timelines Are Set — But Market Conditions Are Difficult

In early 2026, the government officially launched the privatisation process for five major distribution companies. Alvarez & Marsal Middle East, appointed as financial adviser in February 2025, submitted sector-level and enterprise due diligence reports. Investor engagement ran in late January 2026 to test market appetite. The government set hard privatisation deadlines: FESCO by October 2026, GEPCO by November 2026, IESCO by December 2026, and preconditions for HESCO and SEPCO by December 2026.

NEPRA issued a significant warning alongside this plan: under a uniform tariff structure, where all DISCOs charge consumers the same rate, privatisation may not achieve the intended efficiency gains. A private owner managing PESCO, where recovery rates hover near 60%, faces a fundamentally different financial reality than one managing IESCO, where recovery exceeds 95%. The uniform tariff masks those differences and reduces the incentive for a private operator to aggressively cut losses in low-recovery zones.

IPP Renegotiations: Progress With Local Contracts, Stalemate With Chinese

The government renegotiated Power Purchase Agreements with 46 older local IPPs (under the 1994 and 2002 policies) and moved them from take-or-pay to take-and-pay models. During FY 2024–25, PPA terminations and decommissioning of inefficient plants removed 2,829 MW of contracted capacity, reducing the volume of capacity payments owed on idle assets.

Chinese CPEC IPPs remain unrenegotiated. Pakistan’s Privatisation Commission chairman confirmed in mid-2025 that China had not been formally engaged on contract revisions. Beijing has shown no willingness to revise terms. The government’s plan to address renewables-based contracts first, then approach the 2015 Chinese plants, means the largest and fastest-growing portion of the capacity payment bill will remain unchanged for the foreseeable future.

The Rs 200 Billion Equity Injection: Immediate Relief, Not Structural Fix

To ease DISCO liquidity in the short term, the government approved a Rs 200 billion Technical Supplementary Grant structured as equity investment into distribution companies. It prevented several DISCOs from defaulting on their payment chains during the first half of FY 2025–26. But equity injections do not reduce the underlying obligations to IPPs or fuel suppliers. They buy time, which is valuable, but only if structural reforms move faster than the debt accumulates.

NEPRA Tariff Pakistan: What Consumers Can Realistically Expect

The NEPRA tariff that Pakistan consumers pay already reflects a modest reduction compared to the previous cycle. The average national base tariff sits at Rs 33.38 per unit for residential consumers in 2026, slightly down from Rs 34.45 in 2025. The IMF pushed the government to shift the annual tariff rebasing from June to January, starting in 2026, when electricity demand is lower, to soften the seasonal bill shock that occurs when summer rates are set.

However, three forces push against any sustained reduction. First, the Rs 3.23 per unit DSS will remain active for six years. Second, NEPRA-notified tariff reductions are frequently offset by fuel price adjustments (FPAs) that fluctuate monthly. Third, the reduction in government subsidy allocations required under the IMF programme means less fiscal cushion for lower-income slabs. The lifeline tariff (up to 50 units/month) stays fixed at Rs 3.95 per unit, but the moment consumption crosses that threshold, the effective rate jumps sharply.

| Category | Monthly Usage | Base Rate (PKR/kWh) |

|---|---|---|

| Lifeline | Up to 50 units | Rs 3.95 |

| Protected – Slab 1 | 1–100 units | Rs 7.74 |

| Protected – Slab 2 | 101–200 units | Rs 13.01 |

| Unprotected – Slab 1 | 1–100 units | Rs 22.44 |

| Unprotected – Slab 2 | 101–200 units | Rs 23.44 |

| Unprotected – Slab 3 | 201–300 units | Rs 28.27 |

| Unprotected – Slab 4 | 301–700 units | Rs 34.45+ |

| High Consumption | Above 700 units | Up to Rs 62.47 |

Pakistan’s domestic electricity tariff slabs in 2026 range from Rs 3.95 per unit (lifeline consumers, up to 50 units) to Rs 62.47 per unit (high-consumption unprotected consumers above 700 units), as set by NEPRA. Base rates exclude surcharges, FPAs, and taxes.

What Circular Debt Does to Pakistan’s Industries and Jobs?

Academic research focuses on household quintiles. But circular debt carries an equal and less-discussed cost for industry. High electricity tariffs force manufacturers to cut production shifts or move to expensive captive power generation (diesel generators). The Federation of Pakistan Chambers of Commerce and Industry consistently reports electricity costs as the top operational challenge for small and medium enterprises.

Read Also: How Electricity Bills Work in Pakistan

The government saw this clearly. Its push to migrate captive power users onto the national grid in 2025 produced a 35% year-on-year rise in industrial electricity demand between April and August, which directly helped reduce the circular debt flow by boosting DISCO revenues. That linkage is critical: more industrial consumers on the grid means more revenue to cover fixed costs, reducing the share each household must carry.

But load-shedding in PESCO and QESCO regions continues despite Pakistan’s 41,121 MW of operational capacity. Rural industrial clusters, such as the textile mills of Faisalabad, the agricultural machinery manufacturers of Gujranwala, face unscheduled outages that don’t appear in national statistics. Each hour of unplanned outage is an hour of lost output that never comes back.

What Happens If Pakistan Doesn’t Meet IMF Conditions?

The IMF’s Extended Fund Facility for Pakistan explicitly links each tranche of foreign financing to energy sector benchmarks. The Fund acknowledged Pakistan’s “strong FY25 performance” in its December 2025 country report. But it tied that acknowledgement to a direct condition: without timely privatisation milestones and sustained tariff discipline, the gains reverse. Dr. Khaqan Najeeb, former Adviser to Pakistan’s Ministry of Finance, captured the structural problem in precise terms: “The ongoing technical and commercial losses of about 20% highlight inefficiencies in billing, collection, and transmission infrastructure, causing persistent losses projecting to around Rs 600 billion annually.” That Rs 600 billion annual flow is what makes the debt impossible to kill through restructuring alone.

Three specific IMF conditions directly concern circular debt in 2026. First, DISCO recovery rates must rise from 90% (June 2024) to 97.34% by June 2027, a target that requires resolving chronic under-collection in PESCO, HESCO, and SEPCO without politically difficult enforcement operations. Second, the government must meet preconditions for HESCO and SEPCO privatisation by December 2026 — a new structural benchmark the IMF added in 2025. Third, the government must keep the circular debt flow at zero net addition by fiscal year-end — a target that the monthly accumulation data in early 2026 already shows slipping.

Missing these benchmarks does not immediately cut off IMF financing, but it delays the next tranche review and creates pressure to impose harsher conditions. For a government managing foreign exchange reserves on a month-to-month basis, a delayed IMF tranche is not an accounting inconvenience. It is a balance-of-payments risk.

What You Can Actually Do About Your Electricity Bill in 2026?

You cannot personally fix circular debt. But you can control how much of its cost lands on your bill. I have tracked LESCO bills across three years of tariff changes, including the July 2024 slab revision and the January 2025 rate reduction.

The single most expensive mistake I watched households make repeatedly: losing protected consumer status in June because of one high-AC month, then spending the next four months billed at unprotected slab rates of Rs 23–28 per unit instead of Rs 13. That single slip costs a household Rs 3,500–6,000 across the following quarter.

Read Also: How to Reduce Electricity Bill in Pakistan

Here is what actually prevents it:

- Guard your protected consumer status: Stay below 200 units for six consecutive months. Losing this status in June, during peak AC season, can spike your rate from Rs 13 to Rs 23+ per unit and keep you in the unprotected bracket for months after.

- Challenge inflated bills immediately: NEPRA’s SOIR 2024–25 flagged overbilling and detection bills issued without due process as system-wide problems. You have the right to contest any bill through your DISCO’s grievance process and NEPRA’s complaint portal at nepra.org.pk.

- Shift heavy appliances to off-peak hours: Washing machines, irons, and water heaters run the same whether used at 3 PM or 10 PM — but running them outside peak hours reduces demand-linked charges where they apply.

- Calculate your solar payback period honestly: A 2–3 kW system eliminates 80–90% of grid consumption in most Pakistani cities. At current net metering rates and the Rs 3.23 DSS surcharge, the payback period in Lahore, Karachi, and Islamabad has shrunk to 3–4 years for most middle-income households.

- Read the fine print on your bill: Fuel Price Adjustments (FPAs) can swing ±Rs 3–5 per unit month-to-month. Quarterly adjustments are added separately. Understanding these line items helps you spot billing errors before they compound.

Final Thoughts

Circular debt in Pakistan will not disappear through financial engineering alone. The Rs 1.225 trillion bank deal in 2025 was genuinely significant — it converted expensive, opaque Power Holding Limited debt into cheaper, transparent bank financing. The 34% drop in the debt stock during FY 2024–25 was real. These are steps forward, not theatrics.

But steps forward are not the same as solving the problem. Pakistan still pays Rs 2.1 trillion per year in capacity charges for power plants averaging 34% utilisation. No DISCO except TESCO met its T&D loss target in FY 2024–25. CPEC contract renegotiations have not formally begun. The poorest 40% of Pakistani households still carry 55–60% of the system’s non-energy costs on their bills.

As Zafar Masud, Chairman of the Pakistan Banks Association, put it after the September 2025 restructuring: “This is not the end, only a breather. If we lose momentum — if governance reforms stall, if privatisation remains shelved — we will end up back where we started.” That sentence sums up where Pakistan stands in 2026: a moment of genuine reform opportunity that requires sustained political will to become a lasting fix, not just the latest postponement of a problem three decades in the making.

This article was written by Saira Imran She have covered Pakistan’s power sector since 4 years, analysing every Circular Debt Management Plan from 2022 to 2026 and tracking NEPRA tariff determinations.This article draws on NEPRA’s State of Industry Report FY 2024–25, Ministry of Energy Power Division data (April 2026), the IMF Pakistan Country Report (December 2025), and Arif Habib Limited’s monthly circular debt compilations.

Last verified: May 5, 2026 | Full author bio →

FAQs

Circular debt is a chain of unpaid dues across Pakistan’s power supply chain. Distribution companies (DISCOs) fail to collect bills from consumers. Because of that shortfall, they cannot pay power producers. Power producers cannot pay fuel suppliers. The government borrows to fill each gap, and that borrowing rolls back onto every consumer’s bill.

Pakistan’s power sector circular debt reached Rs 1.837 trillion by February 2026, rising Rs 224 billion in just eight months.

The government periodically raises tariffs or imposes surcharges to bridge the deficit instead of fixing structural inefficiencies. Approximately 30–35% of the present electricity tariff consists of non-energy financial adjustments — charges for inefficiency and repayment of debt. Every surcharge added to cover circular debt lands directly on your unit rate, making each kilowatt-hour more expensive than it should be.

ADB research attributes circular debt flows to DISCO inefficiencies (31%), delayed tariff adjustments (35%), financial costs (16%), and unbudgeted subsidies (18%). On top of that, IPP contracts with backstopped payment guarantees, dollar indexation, and high return-on-equity allowances contributed to ever-rising capacity payments.

NEPRA set the average national base tariff at around Rs 33.38 per unit for 2026, a slight reduction from the previous cycle. However, the Rs 3.23 per unit Debt Service Surcharge remains active through a six-year bank loan repayment plan. Meaningful relief requires IPP contract renegotiation and DISCO reform; without both, sustained price reductions are unlikely in the near term.