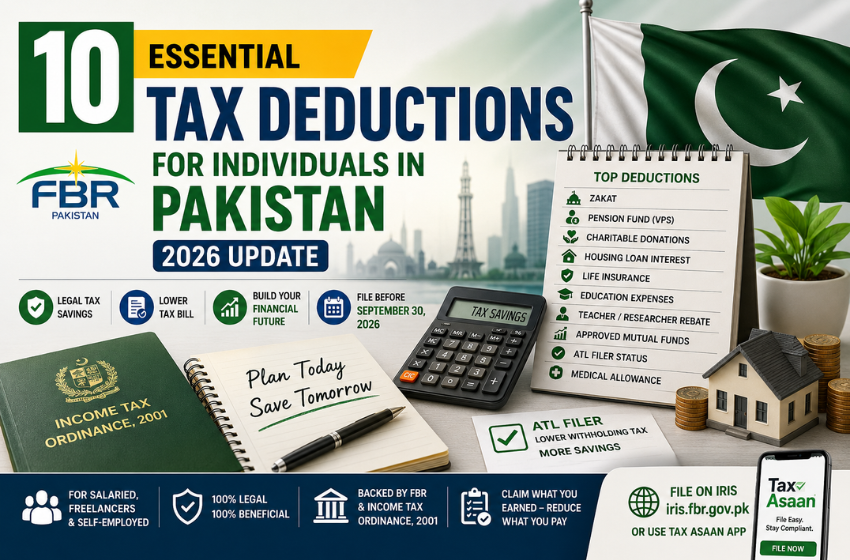

10 Tax Deductions for Individuals in Pakistan 2026

Most salaried Pakistanis pay more tax than they have to. Not because they cheat, but because they never learn which deductions they can legally claim.

The Federal Board of Revenue (FBR) allows several deductions and tax credits under the Income Tax Ordinance, 2001. These reduce your taxable income before the FBR applies any slab rate. That means your tax bill shrinks directly.

The filing deadline for Tax Year 2026 is September 30, 2026. Miss it, and you face penalties plus a 12% annual surcharge on any unpaid tax.

Here are 10 tax deductions for individuals in Pakistan.

1. Zakat Deduction (Section 60)

If your bank deducts Zakat from your savings, you get a straight deduction from your taxable income. No cap, no percentage limit. One condition: you must mark yourself as Muslim on your bank account for automatic Zakat deduction. FBR accepts this without question.

This is one of the easiest tax deductions for individuals in Pakistan. If your bank automatically deducts Zakat, claim it every year.

2. Voluntary Pension Scheme (VPS) Contributions (Section 63)

Contributions to an FBR-approved pension fund are deductible up to PKR 500,000 per year or 20% of your taxable income, whichever is lower.

This one hits hard in a good way for anyone in the higher slabs (25% to 35%). A PKR 300,000 VPS contribution at the 25% rate saves you PKR 75,000 in actual tax. That is real money back in your pocket.

Check if your employer’s provident fund carries FBR recognition. If it does, both employee and employer contributions reduce your taxable salary.

3. Charitable Donations (Section 61)

Donations to approved non-profit organisations earn a tax rebate at your average tax rate. The limit is the lower of your donation amount or 30% of your taxable income.

One small catch: if you donate to an organisation you are personally connected to (an “associate”), the cap drops to 15% of your taxable income.

Before you donate, confirm the organisation holds FBR approval. A donation to a non-approved charity earns you goodwill but zero tax benefit.

4. Medical Allowance Exemption

If your salary structure includes a medical allowance, the FBR exempts up to 10% of your basic salary from tax, with a separate annual cap of PKR 25,000.

Your employer handles this directly when computing monthly withholding. But check your salary slip. Some employers split allowances in ways that do not optimize this exemption. A quick conversation with your payroll department can make a difference.

5. Housing Loan Interest Deduction (Section 64A)

First-time homebuyers get a tax credit on the interest paid on home loans. This applies to houses up to 2,500 square feet or flats up to 2,000 square feet. The eligible loan amount is up to PKR 2 million per year.

The loan must come from a scheduled bank, government, or a regulated financial institution. Private informal borrowing does not qualify.

One important rule: once you claim this credit, FBR blocks you from claiming it on another property for the next 15 tax years. Use it wisely.

6. Life Insurance Premiums (Section 62)

Premiums you pay on life insurance policies qualify for a tax credit. The limit is the lower of the actual premium paid or PKR 150,000 per year.

The credit reduces your calculated tax directly, not just your taxable income. That distinction matters. A credit is stronger than a deduction at the same rupee amount.

Keep your premium receipts. Without them, FBR will not process the claim.

7. Education Expense Credit

Pakistan allows a tax concession on tuition fees paid for children’s education. The deductible amount is up to 20% of your salary or PKR 50,000 per year, whichever is lower.

This applies to accredited schools and institutions. Keep fee receipts and school enrollment records. Informal tutoring or unregistered coaching centres do not qualify.

8. Teacher and Researcher Rebate (25% Tax Rebate)

Full-time teachers and researchers at HEC-recognised institutions or government research bodies receive a 25% rebate on their total calculated salary tax.

That is not a 25% deduction from income. It is 25% off the actual tax amount already computed. For a teacher paying PKR 80,000 in annual tax, this rebate saves PKR 20,000.

Medical professionals who earn from private practice do not qualify for this rebate on that portion of income.

9. Investment in Approved Mutual Funds

Certain growth-oriented and sharia-compliant mutual funds registered with FBR qualify for a tax credit. Check the SECP-approved list before investing.

This deduction works best when you treat it as part of a broader savings plan rather than a last-minute tax move. Invest early in the fiscal year and let returns grow alongside the tax benefit.

10. Filer Status on the Active Taxpayer List (ATL)

This is not a deduction in the traditional sense. But it functions like one across every major financial transaction.

ATL filers pay significantly lower withholding tax on: bank cash withdrawals above PKR 50,000, property purchases and sales, vehicle purchases, dividend income, and bank profit.

Non-filers often pay double the withholding rate. Over a year, especially if you buy a property or car, the savings from filer status easily exceed any single deduction above.

Register on IRIS at iris.fbr.gov.pk or use the Tax Asaan mobile app. Filing for Tax Year 2026 closes on September 30, 2026.

Quick Summary Table for the Tax Deductions for Individuals in Pakistan

| # | Deduction | Limit |

|---|---|---|

| 1 | Zakat | No cap |

| 2 | Voluntary Pension (VPS) | PKR 500,000 or 20% of income |

| 3 | Charitable Donations | 30% of taxable income |

| 4 | Medical Allowance | 10% of basic salary / PKR 25,000 |

| 5 | Housing Loan Interest | PKR 2 million/year |

| 6 | Life Insurance Premium | PKR 150,000/year |

| 7 | Education Expenses | 20% of salary / PKR 50,000 |

| 8 | Teacher/Researcher Rebate | 25% off calculated tax |

| 9 | Approved Mutual Funds | SECP-approved list |

| 10 | ATL Filer Status | Lower WHT across all transactions |

FAQs

Annual income up to PKR 600,000 (PKR 50,000 per month) is fully exempt. You owe zero income tax if your earnings stay below this threshold.

Yes. FBR allows multiple deductions in the same return. Claim every one you qualify for. They do not cancel each other out.

You face a penalty of PKR 1,000 per month of delay (minimum PKR 10,000) plus a 12% annual surcharge on any unpaid tax. You also drop off the ATL, which increases withholding tax rates on your banking and property transactions.

No. Section 64A applies only to a personal house or flat for your own residence. Rental or investment properties do not qualify.